The success of the U.S. residential real estate market, like any other market, is determined by supply and demand. This means we need to look at how many potential purchasers are in the market versus the number of houses that are available to buy.

With early 2020 housing data now rolling in, it’s quite evident there are two big stories impacting this year’s residential real estate market:

1. Buyer demand is already extremely strong

2. Housing supply is at a historically low level

Demand

ShowingTime is a firm that compiles data from property showings scheduled across the country. The latest ShowingTime Showing Index reveals how showings have increased in each of the country’s four regions for five months in a row.

Supply

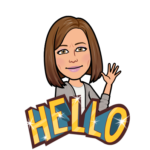

Move.com also just released information indicating that the number of homes currently for sale has declined rapidly and now sits at the lowest level in almost a decade. They explained,

“National housing inventory declined 13.6 percent in January, the steepest year-over-year decrease in more than 4 years, pushing the supply of for sale homes in the U.S. to its lowest level since realtor.com began tracking the data in 2012.”

In response to these numbers, Danielle Hale, Chief Economist at realtor.com, said,

“Homebuyers took advantage of low mortgage rates and stable listing prices to drive sales higher at the end of 2019, further depleting the already limited inventory of homes for sale. With fewer homes coming up for sale, we’ve hit another new low of for sale-listings in January.”

The decrease in inventory impacted every price range, too. Here’s a graph showing the data released by move.com:

Bottom Line

Since there’s a historic shortage of homes for sale, putting your home on the market today could drive an excellent price and give you additional negotiating leverage when selling your house. Let’s get together to determine if listing your house now is your best move.

Content previously posted on Keeping Current Matters

![The Top States Americans Moved to Last Year [INFOGRAPHIC] | Simplifying The Market](https://affinityswfl.com/wp-content/uploads/2020/02/20200207-KCM-Share.jpg)

![The Top States Americans Moved to Last Year [INFOGRAPHIC] | Simplifying The Market](https://affinityswfl.com/wp-content/uploads/2020/02/20200207-MEM-scaled-1.jpg)

![5 Reasons Homeowners Throw Better Parties During the Big Game [INFOGRAPHIC] | Simplifying The Market](https://affinityswfl.com/wp-content/uploads/2020/01/20200131-KCM-Share.jpg)

![5 Reasons Homeowners Throw Better Parties During the Big Game [INFOGRAPHIC] | Simplifying The Market](https://affinityswfl.com/wp-content/uploads/2020/01/20200131-MEM.jpg)