Buying your first home can seem overwhelming. Thankfully, there’s a lot of great information out there to help you feel more confident as you learn about the process. For those in younger generations who aspire to buy, here are three things to consider sooner rather than later in your journey:

1. Understand What it Takes to Purchase a Home

Overall, Millennials make up the largest group of homebuyers in today’s real estate market, and Gen Z is not too far behind. A recent study shared by Freddie Mac shows, however, that Generation Z isn’t as confident in the homebuying process as Millennials. The best thing potential young buyers can do is understand what it takes to buy a home. Learn as much as you can about the mortgage process, down payment options, and the overall steps to take along the way.

2. Realize Your Opportunity to Build Wealth

Homeownership allows you the chance to put a small portion of the home’s value down when you buy, and then watch your appreciation grow on the full value of the home – not just on the down payment. It’s one of the best investments you can make, and a form of ‘forced savings’ working in your favor over time. The added bonus? You get to live there, too.

3. Find Someone You Trust to Help You Through the Process

Having someone you trust to guide you through this process is invaluable. Finding a local real estate expert to help you navigate through the transaction and feel more confident as you make important decisions could be the best choice you make.

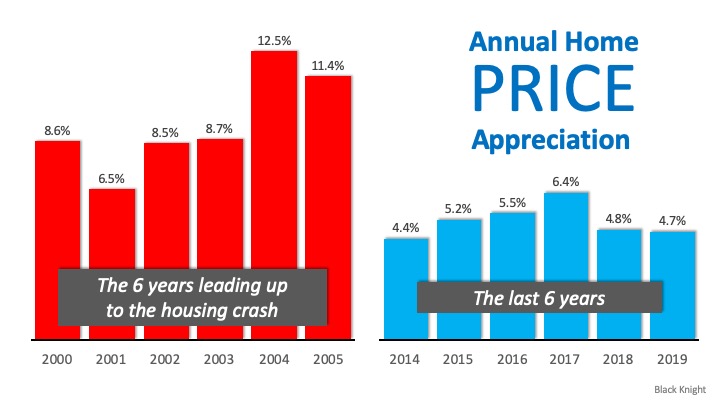

For Millennials and Gen Z’ers thinking about buying, today’s historically low interest rates combined with the outlook for future home appreciation is a big win. This means whatever you buy today, you’ll be bragging about 10 years from now. You can feel confident about that!

Bottom Line

If you’re ready, buying your first home sooner rather than later is one of the best decisions you can make. But there are many things to consider before taking that step, so let’s work together to help you confidently navigate the full journey.

Content previously posted on Keeping Current Matters

![The Difference an Hour Makes [INFOGRAPHIC] | Simplifying The Market](https://affinityswfl.com/wp-content/uploads/2020/03/20200306-KCM-Share.png)

![The Difference an Hour Makes [INFOGRAPHIC] | Simplifying The Market](https://affinityswfl.com/wp-content/uploads/2020/03/20200306-MEM-EN.jpg)

![10 Steps to Buying a Home [INFOGRAPHIC] | Simplifying The Market](https://affinityswfl.com/wp-content/uploads/2020/02/20200228-KCM-Share.jpg)

![10 Steps to Buying a Home [INFOGRAPHIC] | Keeping Current Matters](https://affinityswfl.com/wp-content/uploads/2020/02/20200228-MEM-EN.jpg)